So the fiscal cliff is looming closer and closer, and a new poll shows that “Americans clearly want Washington to solve its looming budget crisis, and they clearly reject almost every option to do that”. It sounds like typical voter stupidity at first, especially since a lot of the options on the table are not only palatable, but probably should be enacted for their own sake. The article lists: “raising taxes on everyone, cutting Medicaid or Medicare spending, raising the age for Medicare, or taking away tax deductions for charitable contributions or home mortgage interest,” and the last three all seem like no-brainers to me.

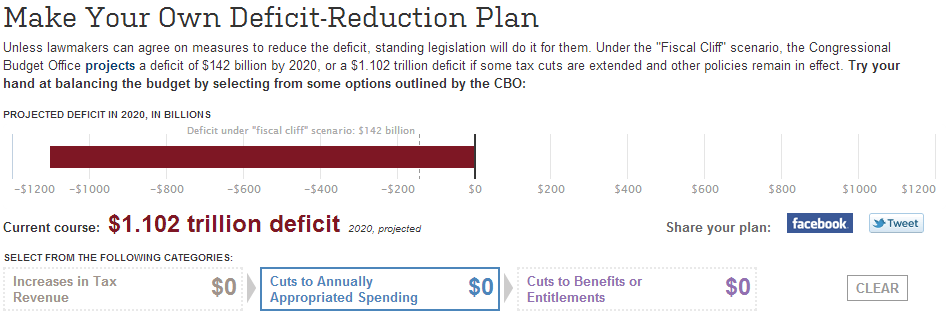

Before you start to feeling too smug, however, you can head over to the Wall Street Journal and try your hand at balancing the budget on your own. You start with the $1,102,000,000,000 10-year deficit and a menu of choices for raising taxes and cutting discretionary and entitlement spending.

I noodled around with it for a while, and it’s surprisingly hard to make that deficit go away without doing things that seem like a bad idea. I think part of that is just the nature of the problem: there’s no easy way out. That’s why I believe chances are very good we’ll go over the fiscal cliff.

There are a couple of other things worth noting, however. The first is that the short-run deficits that we’re facing have a lot to do with the fact that we’re in a recession. The Congressional Budget Office did an estimate, and they found that about one-third of the budget deficit comes directly from the fact that we’re in a recession:

The Congressional Budget Office (CBO) estimates that if those resources were not underutilized—that is, if the economy was operating at its potential level—the projected federal deficit under current law in fiscal year 2012 would be about a third lower, or roughly $630 billion instead of the $973 billion projected in CBO’s most recent baseline. That deficit would be equal to about 4.0 percent of gross domestic product (GDP), compared with the 6.2 percent deficit projected for 2012 in CBO’s baseline. If the economy was operating at its potential, the deficit would be lower because incomes and, therefore, revenues would be higher, while the rate of unemployment and, therefore, outlays for certain government programs would be lower.

Meanwhile the risk of entitlement spending is really less about current levels of spending, and more about future levels of spending. Trying to trim from Medicare or Social Security today in order to fix the short-term budget problems misses the point of the exercise entirely.

While we’re at it, here’s another fun example of why these questions get so complicated. If you look at the “Cuts to Annually Appropriated Spending” section you’ll see this as one of the options: “Increase passenger fees for airport security and air-traffic controls”. Why is increasing fees listed as a spending cut instead of an increase in revenue? That’s just weird.

In any case, here’s my basic take on the situation:

- In the short-run it’s more important to grow the economy than to fix the deficit.

- Entitlement reform should be conducted with an eye towards long-run impacts, not short-run effects. Even so, there will be immediate economic benefits from gradual, long-range reforms because it will ease uncertainty about our fiscal future.

- Tax reform should be conducted primarily with the goal of decreasing distortions in the economy and easing uncertainty, and a secondary goal of raising some additional revenues.

The ideal approach to the recession would have been to set aside major new programs like Obamacare for the time being, focus on stimulus spending that actually grows the economy instead of rewarding political backers, and reform the tax code and entitlements with an eye to the long run, not ending short-run deficits. Now we’ve got conservatives angry about the deficit without any real understanding of the timing of the problem and liberals angry that the rich aren’t paying more in taxes without any appreciation for how bad our tax code really is, and in this confused mess I really can’t see any productive solutions being offered whatsoever.

Anyway: go check out the WSJ page, and let me know how you’d balance the budget or if you just give up in frustration like I did.

I agree with you that fixing the economy is more important in the short run. The issues I have are that it only allows what the CBO offered and I think there are more options out there. It is great as an example of how difficult it is though. Lastly the issue with worrying less about the budget is that when the economy turns around politicians often don’t worry about fixing the budget quite as much. That’s truly what frightens me most.