Some claim that corporate “short-termism“–or what Hillary Clinton called “quarterly capitalism“–has negative effects on the economy. But is there any evidence for the claim? A new McKinsey report answers in the affirmative:

- From 2001 to 2014, the revenue of long-term firms cumulatively grew on average 47 percent more than the revenue of other firms, and with less volatility. Cumulatively the earnings of long-term firms grew 36 percent more on average over this period than those of other firms, and their economic profit grew 81 percent more on average.

- Long-term firms invested more than other firms from 2001 to 2014. Although they started this period with slightly lower research-and-development spending, cumulatively by 2014, long-term companies on average spent almost 50 percent more on R&D than other companies. More important, they continued to increase their R&D spending during the financial crisis, while other companies cut R&D expenditure; from 2007 to 2014, R&D spending for long-term companies grew at an annualized rate of 8.5 percent versus 3.7 percent for other companies.

- Long-term companies exhibit stronger financial performance over time. On average, their market capitalization grew $7 billion more than that of other firms between 2001 and 2014. Their total return to shareholders was also superior, with a 50 percent greater likelihood that they would be in the top decile or top quartile by 2014. Although long-term firms took bigger hits to their market capitalization during the financial crisis than other firms, their share prices recovered more quickly after the crisis.

- Long-term firms added nearly 12,000 more jobs on average than other firms from 2001 to 2015. Had all firms created as many jobs as the long-term firms, the US economy would have added more than five million additional jobs over this period. On the basis of this potential job creation, this suggests, on a preliminary basis, that the potential value unlocked by companies taking a longer-term approach was worth more than $1 trillion in forgone US GDP over the last decade; if these trends continue, it could be worth nearly $3 trillion through 2025.

The report concludes that “the potential value that could have been unlocked had all US publicly listed companies taken a long-term orientation exceeded $1 trillion over the past ten years” (pg. 7).

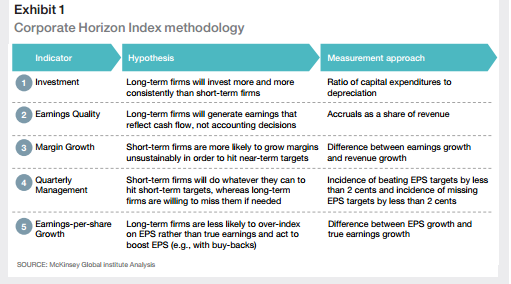

How do the researchers determine that a company is “long-term”? Their Corporate Horizon Index consists of five financial indicators:

In a Harvard Business Review article, the researchers explain,

After running the numbers on these indicators, two broad groups emerged among those 615 large and midcap U.S. publicly listed companies: a “long-term” group of 164 companies (about 27% of the sample), which were either long-term relative to their industry peers over the entire sample or clearly became more long-term between the first half of the sample period and the second half, and a baseline group of the 451 remaining companies (about 73% of the sample). The performance gap that subsequently opened between these two groups of companies offers the most compelling evidence to date of the relative cost of short-termism — and the real payoff that arises from managing for the long term.

…While we can’t directly measure the cost of short-termism, our analysis gives an indication of just how large the value of what’s being left on the table might be. As noted earlier, if all public U.S. companies had created jobs at the scale of the long-term-focused organizations in our sample, the country would have generated at least five million more jobs from 2001 and 2015 — and an additional $1 trillion in GDP growth (equivalent to an average of 0.8 percentage points of GDP growth per year). Projecting forward, if nothing changes to close the gap between the long-term group and the others, then the U.S. economy could be giving up another $3 trillion in foregone GDP and job growth by 2025. Clearly, addressing persistent short-termism should be an urgent issue not just for investors and boards but also for policy makers.

How we manage matters.