A few years ago, researchers from Harvard, Wharton, Kellogg, and the University of Arizona argued that goal setting was “overprescribed” and featured “powerful and predictable side effects” (pg. 6). While acknowledging past research demonstrates that “specific goals provide clear, unambiguous, and objective means for evaluating…performance” and thus “motivate performance far better than “do your best” exhortations” (pg. 7), the researchers found that this intensity of focus on goals can lead to tunnel vision and poor, often unethical decisions. Examples include Sears in the early 1990s, whose sales goals for its auto repair staff led to overcharging and unnecessary repairs. Revenue-based rather than profit-based goals at Enron helped lead to the company’s destruction. A challenging goal (a car “under 2,000 pounds and under $2,000”) coupled with a tight deadline at Ford in the late 1960s brought about the easily-combustible Pinto, many deaths and injuries, and expensive lawsuits. These narrow goals crowded out not only ethical behavior, but the broader purpose of the goals themselves. Quality, in essence, is often sacrificed for the quantifiable. Short-term gains are pursued rather than long-term health and growth. Furthermore, such narrow goals create “a focus on ends rather than means…[The researchers] postulate that aggressive goal setting within an organization increases the likelihood of creating an organizational climate ripe for unethical behavior“(pg. 10). Narrow goals decrease satisfaction, even with high-quality outcomes, which have negative effects on future behavior. They can also inhibit learning and experimentation with alternative methods, undermine cooperation, and harm intrinsic motivation.

Goal setting is often a subject of discussion about behavioral ethics and internal programs. We’ve seen in recent cases such as at Wells Fargo and Volkswagen how cheating and lying become the norm when performance goals are not reasonably achievable. Recent evidence in a paper by Niki den Nieuwenboer, João da Cunha, and ES collaborator Linda Treviño shows the internal dynamics and processes that lead directly to cheating behaviors.

The researchers, one of which was embedded inside the company, observed managers and sales staff over 15 months at a large (10,000 employees) telecommunications company. The company had established goals for its desk sales teams designed to motivate productivity, including a target for sales as well as sales-related work, such as making cold calls to customers, and gathering information about potential customers, among other planning activities.

For the senior leaders at the company, these targets were part of a broader– and cost-lowering — strategy of shifting sales staff from the field towards desk jobs. The field staff cost the company $225 more per customer contact than the sales teams working at desks. The aim was thus to incentivize desk people to improve efficiency and reduce costs in the long-run.

However, because the desk sales team cheated the internal systems, the company didn’t actually gain the cost savings that it thought it had. The apparent success of the desk sales team (based on false information) led to upper management reducing the number of field staff sales numbers, which undermined an important sales channel at the firm.

The misconduct was uncovered inadvertently. Originally, one of the researchers was embedded inside the company to observe the implementation of a sales-related IT system. As he observed and interviewed employees about their use of the system, the scope of the research was soon expanded to include unethical behaviors. He observed that both middle managers and frontline sales staff were aware that the sales goals were unreachable, and that sometimes sales staff tried to push back on pressure from their managers. When sales targets didn’t budge, the managers got creative to solve their goals, devising strategies to induce the sales staff to cheat the internal systems. Manager pay was directly tied to whether their direct reports met performance goals hence the need to game the system to safeguard their income.

The managers took advantage of “structural vulnerabilities” in the system. For example, they changed rules such as expanding the definition of “sales calls” so that more types of calls counted towards that goal – case in point, they counted internal calls and emails as “external” sales calls. Some also just logged fictitious information for calls that never occurred. Other manipulations involved devising IT and administrative schemes that allowed the desk sales teams to take credit for work done by the field sales teams. Additionally, to satisfy the requirement that sales plans be developed for customers, some simply were told to copy and paste plans across various customers, because they knew that very few of them would actually be verified.

Manipulating strategies to meet targets became the norm at the organization. While employees in the unit were aware of these practices, the managers worked to ensure that word of the deceptive practices didn’t get out to senior leaders or to other units.

Because managers and workers apply different skills, the best workers may not be the best candidates for managers. When this is the case, do firms promote someone who excels in her current position, or someone who is likely to excel as a manager? If firms promote based on current performance, then firms may end up with worse managers. Yet if firms promote based on traits that predict managerial potential, then firms may pass over higher performing workers, weakening the power of promotions to encourage workers to perform well in their current roles. Such promotion policies could also lead to perceptions of favoritism, unfairness, or that succeeding in one’s job goes unrewarded.

Using detailed microdata on sales workers in US firms, we provide the first large scale empirical evidence suggesting that firms prioritize current performance in promotion decisions at the expense of promoting the best potential managers. Our findings are consistent with the “Peter Principle,” which, in its extreme form, states that firms promote competent workers until they become incompetent managers (Peter and Hull 1969).

…Overall, our empirical findings are consistent with the Peter Principle: firms promote based on current job performance even though pre-promotion sales negatively predicts managerial performance and other observable characteristics positively predict managerial performance. We caution that our results do not imply that firms use suboptimal promotion policies or have mistaken beliefs. Promotion policies that favor strong sales performance may provide a variety of incentive benefits that justify the costs of managerial mismatch. For example, promoting based on current job performance may help preserve tournament incentives (Lazear and Rosen 1981). Prioritizing objective performance measures in promotions may also improve incentives by avoiding favoritism (Prendergast 1998) and maintaining fairness norms. Promotion policies based on verifiable performance metrics such as sales may also discourage the manipulation of other, more fungible performance metrics such as credit sharing and collaboration experience (DeVaro and Gurtler 2015). What our results do show is that the costs of not promoting the best potential managers are high: our estimates suggest that firms are willing to forgo up to a 30% improvement in subordinate performance to achieve better incentives or to avoid costly politicking.

…This study offers the first empirical tests of the Peter Principle using data on promotions across a large number of firms. Although theoretical work and reviews have hypothesized that promotions based upon current job performance may yield managerial mismatch (Fairburn and Malcomson 2001; Waldman 2003; Lazear 2004), scant empirical research has tested the Peter Principle directly. Our work is most closely related to Grabner and Moers (2013), which shows that a bank places less weight on current job performance when a promotion would be to a job performing dissimilar tasks. However, Grabner and Moers uses data from a single firm and does not attempt to estimate the cost of the Peter Principle. Understanding the costs associated with the Peter Principle is important because it helps explain a variety of organizational practices, such as the use of parallel job ladders for individual contributors and managers, or the use of separate evaluation criteria for performance (which are often tied to bonuses) and potential (which are often tied to promotions) (pgs. 1-5).

Being a good worker does not mean one will be a good manager.

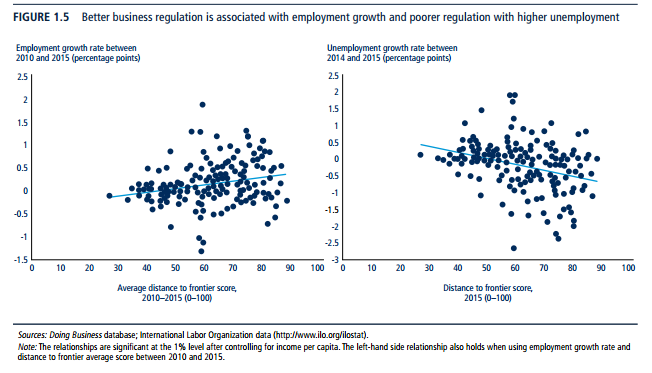

The World Bank’s latest Doing Business report is out (check out last year’s). The report “measures regulations affecting 11 areas of the life of a business. Ten of these areas are included in this year’s ranking on the ease of doing business: starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting minority investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency. Doing Business also measures labor market regulation, which is not included in this year’s ranking.”

Economies in all regions are implementing reforms easing the process of doing business, but Europe and Central Asia continues to be the region with the highest share of economies implementing at least one reform—79% of economies in the region have implemented at least one business regulatory reform, followed by South Asia and Sub-Saharan Africa.

The report features four case studies in the areas of starting a business, dealing with construction permits, registering property and resolving insolvency, as well as an annex on labor market regulation. See all case studies.

The report finds that

one of the mechanisms through which business regulation can impact employment directly is the simplification of business start-up regulations. Across economies there is a significant positive association between employment growth and the distance to frontier score (figure 1.5).[ref]”Doing Business measures many different dimensions of business regulation. To combine measures with different units such as the number of days to obtain a construction permit and the number of procedures to start a business into a single score, Doing Business computes the distance to frontier score. The distance to frontier score captures the gap between an economy’s current performance and the best practice across the entire sample of 41 indicators across 10 Doing Business indicator sets. For example, according to the Doing Business database across all economies and over time, the least time to start a business is 0.5 days while in the worst 5% of cases it takes more than 100 days to incorporate a company. Half a day is, therefore, considered the frontier of best performance, while 100 days is the worst. Higher distance to frontier scores show absolute better ease of doing business (as the frontier is set at 100 percentage points), while lower scores show absolute poorer ease of doing business (the worst performance is set at 0 percentage points). The percentage point distance to frontier scores of an economy on different indicators are averaged to obtain an overall distance to frontier score” (pg. 5).[/ref]While this result shows an association, and cannot be interpreted in a causal fashion, it is reassuring to see that economies with better business regulation, as measured by Doing Business, also tend to be the economies that are creating more job opportunities. When it comes to unemployment, the expected opposite result is evident. Economies with less streamlined business regulation are those with higher levels of unemployment on average. In fact, a one-point improvement in the distance to frontier score is associated with a 0.02 percentage point decline in unemployment growth rate.

…The data support this interpretation as there is a strong association between inequality, poverty and business regulation. In fact, economies with better business regulation have lower levels of poverty on average. Indeed, a 10 percentage point improvement in the distance to frontier is associated with a 2 percentage point reduction in the poverty rate, measured as the percentage of people earning less than $1.90 a day. Fragility is also a factor linked to poverty. However, even fragile economies can improve in areas that ultimately reduce poverty levels (pg. 7-8).

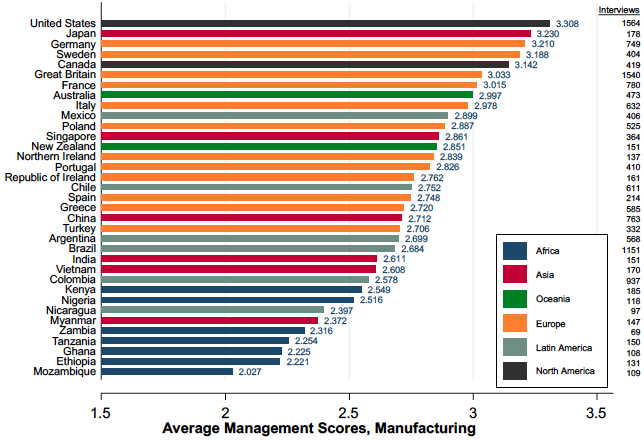

The graph above comes from a recent post by MIT economist John Van Reenen, who has been doing research on the economics of management for the last 15+ years.[ref]Reenen’s work was the foundation of my GBR article.[/ref] He explains,

Many case studies illustrate the importance of management. For example, one I was involved with was Gokaldas Exports (Bloom et al. 2013), a family-owned business founded in 1979 that had grown into India’s largest apparel exporter by 2004. It had 35,000 workers, was valued at approximately $215 million, and exported nearly 90% of its production. Its founder, Jhamandas H Hinduja, had bequeathed control of the company to three sons, each of whom brought in his own son. Nike, a major customer, wanted Gokaldas to introduce lean management practices and put the company in touch with consultants who could help to make this happen. But the CEO was resistant. It took rising competition from Bangladesh, multiple demonstration projects, and finally the intervention of other family members (one of whom I taught in business school) to overcome this resistance. The new practices led to greatly enhanced performance.

Reenen’s work on the World Management Survey has shown that “large, persistent gaps in basic managerial practices…are associated with large, persistent differences in firm performance. Better-managed firms are more productive, grow at a faster pace, and are less likely to die…We performed a simple accounting exercise to evaluate the importance of management for the cross-country differences in productivity. We found that management accounted for about 30% of the unexplained TFP differentials driving the large differences in the wealth of nations.” He concludes,

As our Gokaldas case study mentioned above illustrated, many firms in developing countries may not even realise how weak their management practices are. Or, even when they do they realise this, they may not know how to improve things. Tools such as benchmarking and training can help spread information and knowledge in both of these dimensions. Governments and NGOs often do this, but such programmes are rarely evaluated in a rigorous way (for a survey, see McKenzie and Woodruff 2017). Doing so may be able to raise management and ultimately the wealth of emerging nations.

When a random sample of American adults were asked the question “Just a rough guess, what percent profit on each dollar of sales do you think the average company makes after taxes?” for the Reason-Rupe poll in May 2013, the average response was 36%! That response was very close to historical results from the polling organization ORC International polls for a slightly different, but related question: What percent profit on each dollar of sales do you think the average manufacturer makes after taxes? Responses to that question in 9 different polls between 1971 and 1987 ranged from 28% to 37% and averaged 31.6%.

How do the public’s estimates of corporate profit margins compare to reality? Not surprisingly they are off by a huge margin. According to this NYU Stern database for more than 7,000 US companies (updated in January 2018) in many different industries, the average profit margin is 7.9% for all companies and 6.9% for more than 6,000 companies excluding financials…Interestingly, for nearly 100 industries analyzed by NYU Stern, there’s only one industry that had a profit margin as high as 36% – and that was tobacco at 43.3%. The next highest profit margin was 26.4% for financial services, but more than 72% of industry profit margins were single-digits and the median industry profit margin is 6%.

“Big Oil” companies make a lot of profits, right? Well, that industry (Integrated Oil/Gas) had a below-average profit margin of 5.6% in the most recent period analyzed, and separately, the Production and Exploration Oil/Gas industry is losing money, reflected in a -6.6% profit margin. For the general retail sector, the average profit margin is only 2.3% and for the grocery and food retail industry, it’s even lower at only 1.6%. And evil Walmart only made a 2.1% profit margin in 2017 (first three quarters) which is less than the industry average for general retail, possibly because grocery sales now make up more than half of Walmart’s revenue and profit margins are lower on food than general retail. Interestingly, Walmart’s profit margin of 2.1% is actually less than one-third of the 6.5% the average state/local government takes of each dollar of Walmart’s retail sales for sales taxes. Think about it – for every $100 in sales for Walmart, the state/local governments get an average of $6.50 in sales taxes (and as much as $10.12 in Louisiana and $9.45 in Tennessee, see data here), while Walmart gets only $2.10 in after-tax profits!

Perry concludes, “The public’s complete overestimation of how much companies earn in profits as a share of sales explains a lot…The general public that believes in the fantasy-world of unrealistically, sky-high 36% profit margins would naturally think companies are just being greedy and stingy when they don’t pay higher “living wages” and have to be forced to do so through minimum wage legislation. If the average person could realize that a 36% profit margin isn’t even close to reality and that the typical, median firm has a profit margin of only less than 8% or almost 30 percentage points below what the public thinksis a normal profit margin, then hopefully the average person would become a little more realistic about how the business world operates. Companies aren’t being stingy when they pay competitive wages, they’re just trying to survive on what are sometimes razor-thin profit margins, in a competitive environment where there’s not a large margin of error.”[ref]Perry also has a great post and WSJ article about CEO pay.[/ref]

corporate social responsibility (CSR) activities can lead to higher future productivity…These findings complement previous research that finds “that firms can strategically engage in socially responsible activities to increase private profits. Given that the firm’s stakeholders may value the firm’s social efforts, the firm can obtain additional benefits from these activities, including: enhancing the firm’s reputation and the ability to generate profits by differentiating its product, the ability to attract more highly qualified personnel or the ability to extract a premium for its products.”

It’s important to emphasize that companies must “strategically engage” in CSR activities in order for them to be beneficial. In other words, not all CSR activities are created equal and, as should be clear from the bulk of the article, what truly helps society is managing well. In fact, recent research suggests that CSR activities can lead to employee misconduct:

In this paper, we explore another supply-side channel through which CSR can affect profitability: the impact on employee misbehavior on the job. Employee misbehavior is a common and costly problem facing businesses and organizations. It has been estimated that companies lose about 5% of their annual revenues to various forms of internal fraud (Association of Certified Fraud Examiners, 2016). A survey from the National Retail Federation (NRF) reports that in the retail industry alone, employee theft amounted to $15 billion (over a third of the total inventory shrinkage) in 2014 (NRF, 2015). Another survey reports that in 2015, one in every 38 employees in the retail industry was apprehended for theft from their employers (pg. 2).

They explore the possible effects of CSR through two channels:

“First, [CSR] can serve as a social incentive tool for motivating workers to reduce unethical and counterproductive behavior on the job. Previous studies have shown that, consistent with the standard gift-exchange model, workers reciprocate a higher wage from their employer by reducing misbehavior on the job that hurts the employer (Flory, Liebbrandt, & List, 2016; Ockenfels, Sliwka, & Werner, 2015). Similar to how monetary-incentives reduce worker misbehavior through a gift-exchange mechanism, social incentives in the form of CSR may reduce misbehavior, by triggering reciprocity towards the employer. CSR may thus reduce worker misbehavior through the gift-exchange channel” (pgs. 2-3).

“A second channel is that CSR can increase worker misbehavior through moral-licensing. Prosocial behavior is motivated in part, by self- (and social-) image motives: people act prosocially, in part to signal to themselves (and to others) that they are good and moral individuals (Benabou and Tirole 2006, 2011). While prosocial deeds can boost individual self-image, unethical behavior can damage it. As our moral standards are constantly challenged in multiple dimensions, good behavior in one domain may liberate us to behave unethically in another domain. Such a dynamic of moral licensing in individual behavior has been documented in the social psychology literature” (pg. 3).

“To shed empirical evidence into our theory,” the authors write,

we conduct a natural field experiment with over 3000 workers who we hired ourselves. In this manner, we served as the employer of an online labor market platform (Amazon Mechanical Turk) and invited interested workers to our website to perform a short transcription task for payment. The task and the payment structure were designed in a manner that provided opportunities for workers to misbehave. For example, all workers in our experiment received 10% of their total payment upfront, and immediately upon accepting the contract, and received the remaining 90% of their wage, once they completed the task. Receiving a percentage of the wage upfront creates an incentive for workers to accept the contract without actually working on, or completing the task. To provide the necessary variation to identify the critical pieces of the model, we randomized workers’ into one of the 6 treatments, across which we varied wage, CSR incentive, and the framing and timing of the CSR message (pg. 3).

Their results?

Overall, our results suggest that our usage of CSR increased cheating. First, the share of workers who shirk their primary job duty increases significantly –by roughly 20%– from the baseline to our CSR treatments. Indeed, CSR not only increases the number of people who misbehave, it also increases the level of shirking: the average level of cheating by workers increases by 11%. Second, consistent with the moral-licensing effect of CSR, we find the share of cheaters to be the highest when we frame CSR as a prosocial act on behalf of workers. While CSR increases cheating, we do not find any effect on the average quality of work after accounting for the cheating. We also do not find any differences in cheating behavior across workers who could and could not sort themselves into the CSR job. We argue that our inability to document any selection effect may be due to the relatively high rate of accepting the contract by our workers in all treatments.

…As we decrease the wage and increase the expenditure on CSR, we find the share of cheaters to increase considerably. In other words, we find that substituting just about 5% of the wage with CSR increases the share of cheaters by 25%, while substituting 28% of wage with CSR increases the share of cheaters by over 50%. Likewise, the intensity of cheating per worker increases as well (pg. 4).

In short,

our results reveal a potential dark side to the supply-side effect of CSR. We find that CSR can increase worker misbehavior on the job by generating a moral-licensing effect. Our findings also have important implications on how employers should communicate CSR initiatives to their employees. Importantly, we find some suggestive evidence that the way CSR is communicated to workers can play an important role in the extent to which it leads to moral licensing. When communicated to the employees as a benevolent act that the employer engages in, on workers’ behalf, CSR is (marginally insignificantly) more likely to exploit workers self-image and to lead to less moral choices in the future. This result is consistent with the findings of Kouchaki and Jami (2016) who document a higher level of moral-licensing, when consumers are exposed to a CSR message that praises the consumers compared to a message that praised the company for CSR (pg. 4).

This is why my GBR article focused on good management. This does far more good than image-boosting CSR activities. As business ethicist Chris MacDonald explains, businesses contribute to society by making useful products or providing useful services, providing employment, providing investment opportunities for investors, obeying laws and regulations, and paying taxes. CSR, according to MacDonald, misunderstands capitalism, acts as a smokescreen, and squanders public/activist/media attention:

The central tenet of CSR — namely that the best way for business to contribute socially is through good works — is faulty, and implies a misunderstanding of the basic wealth-and-welfare generating function of markets. Businesses contribute by producing things we want; they facilitate voluntary exchanges of goods and services that, when conducted honestly, leave all concerned better off. (Ask yourself: when did Bill Gates start contributing to society? Was it in 1994, when he founded the Bill & Melinda Gates Foundation? Or was it in, say, 1975, when Gates founded the firm — Microsoft — that would help put the power of computers in of millions of offices and homes?

…When business leaders start bragging about their CSR activities, we should smile politely, and then enquire how their companies are doing in terms of honest advertising, corporate governance and regulatory compliance.

In the face of corporate scandals and economic instability, what we ought to be asking of business executives is that they focus on doing their job honestly and diligently. In any given week, millions of dollars are being spent on academic and industry conferences, round-tables, and dinners to talk about the importance of CSR. In any given week, newspaper stories are being drafted about which companies are doing well, or badly, in their CSR efforts. And in any given week, activists are staging protests, writing letters, and educating the public about the failures of companies to be “socially responsible.” What would happen, I wonder, if all of that money and effort were redirected to the simple idea of getting more people, in more businesses, to behave more consistently according to basic rules of honesty and integrity?

I think this fits pretty well with the overall theme of my article: do your job. And do it well.

At least according to a report by the non-profit research organization JUST Capital. As detailed in Forbes,

JUST Capital polls, on a continuous basis, more than 50,000 Americans, asking them over and over again a series of simple questions on what makes for a just company: Is pollution important? Are wages important? Do benefits matter?

These polls determine how JUST Capital measures corporate justness. The metrics range from worker pay and worker treatment, to leadership and ethics, job creation, customer treatment, supply chains and environmental performance. JUST Capital then proceeds to apply these metrics to individual companies to determine the most just companies in the nation — the 100 highest-ranking in measures of fair and responsible corporate behavior within its ranking of the largest 897 publicly-traded firms in the U.S.

Here’s what its most recent study found: Stock market indexes based on the leaders of JUST Capital’s 2016 rankings outperformed the Russell 1000 index throughout the decade ending in 2016 within a range of 1-4 percentage-points.

Most of these companies also:

• Generated 3.5% higher 5-year Return on Invested Capital.

• Pay roughly 20% more workers a living wage

• Have almost 17% more women board members

• Created 1.8x more jobs in America

• Provide employees more flexible working hours and paid time off

• Pay 8x fewer consumer-related fines

• Recycle about 3x more waste in % terms

• Are 2x more likely to have sound supply chain policies

• Donate about 2x as much of their profit to charity

The piece concludes,

What this all amount to is more than simply an exhortation to the American private sector to “do the right thing.” It’s not just a wake-up call to “do what’s best for your company long-term” but most importantly, it will do what will get this country booming for the top 20 percent of Americans as well as Wall Street. Our markets need the sort of demand our American consumers can fulfill with money they’ve earned — we need their spending power to drive all the growth we’re capable of creating. And to spend, they need to earn. Enlightened CEOs will making sure their employees will earn fair wages importantly because they are the true value creators of the 21stcentury.

At the Ethical Systems blog, they mention Milton Friedman’s (in)famous 1970 essay in connection with this report:

In 1970 Milton Friedman wrote a now famous essay in theNY Times Magazine declaring that the social responsibility of business is to increase its profits. Since then, writers and researchers have been debating whether this accurately reflects the responsibilities of business in society. In the decade since the Global Financial Crisis these debates have become particularly critical, with some participants questioning the basic principles of free market capitalism and whether they serve our current societal needs.

But what if the best way to do right by shareholders was to run a socially responsible business?

What’s funny is that Friedman wouldn’t object, as he clarified in a 2005 Reason essay. Comparing his and Whole Foods’ John Mackey’s philosophy, Friedman writes,

Here is how Mackey himself describes his firm’s activities:

1) “The most successful businesses put the customer first, instead of the investors” (which clearly means that this is the way to put the investors first).

2) “There can be little doubt that a certain amount of corporate philanthropy is simply good business and works for the long-term benefit of the investors.”

Compare this to what I wrote in 1970:

“Of course, in practice the doctrine of social responsibility is frequently a cloak for actions that are justified on other grounds rather than a reason for those actions.

“To illustrate, it may well be in the long run interest of a corporation that is a major employer in a small community to devote resources to providing amenities to that community or to improving its government….

“In each of these…cases, there is a strong temptation to rationalize these actions as an exercise of ‘social responsibility.’ In the present climate of opinion, with its widespread aversion to ‘capitalism,’ ‘profits,’ the ‘soulless corporation’ and so on, this is one way for a corporation to generate goodwill as a by-product of expenditures that are entirely justified in its own self-interest.

“It would be inconsistent of me to call on corporate executives to refrain from this hypocritical window-dressing because it harms the foundations of a free society. That would be to call on them to exercise a ‘social responsibility’! If our institutions and the attitudes of the public make it in their self-interest to cloak their actions in this way, I cannot summon much indignation to denounce them.”

…Finally, I shall try to explain why my statement that “the social responsibility of business [is] to increase its profits” and Mackey’s statement that “the enlightened corporation should try to create value for all of its constituencies” are equivalent.

Note first that I refer to social responsibility, not financial, or accounting, or legal…Maximizing profits is an end from the private point of view; it is a means from the social point of view. A system based on private property and free markets is a sophisticated means of enabling people to cooperate in their economic activities without compulsion; it enables separated knowledge to assure that each resource is used for its most valued use, and is combined with other resources in the most efficient way.

Of course, this is abstract and idealized. The world is not ideal. There are all sorts of deviations from the perfect market–many, if not most, I suspect, due to government interventions. But with all its defects, the current largely free-market, private-property world seems to me vastly preferable to a world in which a large fraction of resources is used and distributed by 501c(3)s and their corporate counterparts.

A lotofresearch suggests that those who speak the most in groups tend to emerge as leaders.

But does it matter who speaks up, or how they do it? In a forthcoming article in Academy of Management Journal, my colleagues Elizabeth McClean, Kyle Emich, and Todd Woodruff and I share how we explored these questions in two studies. We found that those who speak up can gain the respect and esteem of their peers, and that increase in status made people more likely to emerge as leaders of their groups — but these effects happened only for some people and only when they spoke up in certain ways. Specifically, speaking up with promotive voice (providing ideas for improving the group) was significantly related to gaining status among one’s peers and emerging as a leader. However, speaking up with prohibitive voice (pointing out problems or issues that may be harming the team and should be stopped) was not. We further found that the gender of the person speaking up was an important consideration: The status bump and leader emergence that resulted from speaking up with ideas only happened for men, not for women.

The researchers studied cadets at the United States Military Academy at West Point and Master Workers on Amazon Mechanical Turk:

Participants were randomly assigned to one of four conditions, in which they listened to an audio recording of (1) a man speaking up with an idea for improving the process, (2) a woman speaking up with an idea for improving the process, (3) a man pointing out a problem with the process, or (4) a woman pointing out a problem with the process. Participants then rated how much status they perceived the speaker to have in the group and answered several questions about how effective the speaker was in influencing the team (a common method of assessing leadership emergence).

Across both studies—using both field and experimental research designs and very different populations of respondents—we saw the same pattern of results: Men who spoke up with ideas were seen as having higher status and were more likely to emerge as leaders. Women did not receive any benefits in status or leader emergence from speaking up, regardless of whether they did so promotively or prohibitively. Neither men nor women who spoke up about problems suffered a loss of status or had a lower likelihood of emerging as a leader (though they weren’t helped by speaking up, either). Also of note, men and women both ascribed more status and leadership emergence to men who spoke up promotively, compared with women who did so.

The researchers suggest,

Virtually every corporate meeting

Managers who want to promote gender equity on their team — or who just want to make sure they are getting as many good suggestions from their team members as possible — will have to proactively work to counteract the tendencies uncovered in our research. After all, one interpretation of this study is that women, even when they speak up and “lean in,” still may not get equal credit for doing so. And if that is the case, then it is essential not only for women to speak up but also for those around them to give equal weight to what they say.

One way to address this challenge would be for managers to amplify women’s ideas by intentionally giving extra attention to their suggestions. After all, if our natural tendency is to give less recognition to women’s ideas, then we will need to make an extra effort to overcome this bias. And given that women are interrupted more often than men are when speaking up in groups, we suggest managers be vigilant about ensuring that equal respect is shown to women when they are voicing their ideas.

Another approach is to document ideas in real time in order to ensure appropriate credit and recognition is given to each one. Some simple ways to do this would be to write ideas on a whiteboard and note whose idea it is, or to have an email folder for suggestions where people’s ideas can be saved electronically.

Lastly, managers should make it a point to call on women in meetings to hear their input, or to find less formal contexts to ask for women’s improvement-oriented suggestions. These recommendations may also help address another longstanding issue regarding women and voice: that women tend to speak up less in mixed-gender settings.

I’ve written about the negative effects of corporate “short-termism” before. A new study takes a look at the criticisms of short-term incentives. The researchers explain,

Critics of short-term incentives argue that they lead the CEO to take myopic actions that boost the short-term stock price at the expense of long-run value. These critics however, rarely back this up with rigorous evidence. This is partly confirmation bias – willingness to accept ‘evidence’ that confirms one’s prior belief, no matter how flimsy. Since the current political environment is distrustful of businesses, people may be more willing to accept ‘evidence’ that CEOs act in ways that destroy value for personal gain. For example, a recent McKinsey study showed that firms that invested more have enjoyed superior long-run returns, and interprets this finding as “finally, evidence that managing for the long term pays off” (Barton et al. 2017).

…In our most recent work on the topic (Edmans et al. 2017b), we study the long-term consequences of short-term incentives by examining two corporate actions with similarities to investment cuts, but whose long-run consequences could be measured more accurately:

Repurchases: These boost the short-term stock price (Ikenberry et al. 1995). CEOs with short-term concerns might have incentives to undertake them. Also like investment cuts, repurchases can either be myopic (if financed by scrapping valuable projects) or efficient (if financed by free cash that would otherwise have been wasted). The long-term stock return measures the return that the firm obtains from the repurchased stock. So, unlike investment cuts, the long-term stock return can be used to diagnose the value implications of the repurchase, even if the return was not caused by the repurchase.

M&A: This has different advantages to repurchases. First, M&A has an announcement date, allowing us to cleanly calculate short- and long-term returns. Second, M&A is a much more significant event than an investment cut (or repurchase) – it is arguably the most transformative corporate decision that a firm can undertake – and so it is likely that at least a significant portion of long-run stock returns would be attributable to the M&A. Indeed, prior research (e.g. Agrawal et al. 1992) has used long-run stock returns to assess the long-term value implications of M&A.

Studying “the relationship between vesting equity and repurchases, and vesting and M&A announcements, between 2006 and 2015,” the researchers found that

a one-standard-deviation increase in vesting equity is associated with a 1.2% increase in a firm’s likelihood of conducting a share repurchase in a given quarter, compared to the unconditional repurchase probability of 37.5%. This translates into $6.16m annualised, compared to the finding in Edmans et al. (2017a) of an annualised fall in investment of $1.8m. While economically meaningful, this magnitude is also plausible: a too-large, myopic repurchase may have prompted the board to step in and block it. We find similar results for M&A. A one-standard deviation increase in vesting equity is associated with a 0.6% increase in a firm’s likelihood of announcing an M&A in a given quarter, compared with the unconditional probability of 15.8%.

…A one-standard-deviation increase in vesting equity is associated with an annualised 0.61% higher return over the two quarters surrounding a repurchase, but a 1.11% (0.75%) lower return during the first (second) year after the repurchase. For M&A, the negative association with long-run returns persists for longer. A one-standard-deviation increase in vesting equity is associated with an annualised 1.47% higher return over the two quarters surrounding an M&A announcement, but a 0.81%, 0.35% (insignificant), 0.72%, and 0.62% lower return in the first, second, and third, and fourth subsequent years.

They conclude,

The results are consistent with Graham et al. (2005), who used a survey to find that 78% of executives would sacrifice long-term value to meet earnings targets. We studied a CEO’s actual behaviour and found that short-term incentives indeed have negative long-term consequences. The current debate on CEO pay typically focuses on how big it is. As a consequence, in the UK and US, there will soon be disclosure of pay ratios. Our results suggest that the horizon of CEO incentives is a more important dimension to reform.

A few years ago, researchers from Harvard, Wharton, Kellogg, and the University of Arizona argued that goal setting was “overprescribed” and featured “powerful and predictable side effects” (pg. 6). While acknowledging past research demonstrates that “specific goals provide clear, unambiguous, and objective means for evaluating…performance” and thus “motivate performance far better than “do your best” exhortations” (pg. 7), the researchers found that this intensity of focus on goals can lead to tunnel vision and poor, often unethical decisions. Examples include Sears in the early 1990s, whose sales goals for its auto repair staff led to overcharging and unnecessary repairs. Revenue-based rather than profit-based goals at Enron helped lead to the company’s destruction. A challenging goal (a car “under 2,000 pounds and under $2,000”) coupled with a tight deadline at Ford in the late 1960s brought about the easily-combustible Pinto, many deaths and injuries, and expensive lawsuits. These narrow goals crowded out not only ethical behavior, but the broader purpose of the goals themselves. Quality, in essence, is often sacrificed for the quantifiable. Short-term gains are pursued rather than long-term health and growth. Furthermore, such narrow goals create “a focus on ends rather than means…[The researchers] postulate that aggressive goal setting within an organization increases the likelihood of creating an organizational climate ripe for unethical behavior“ (pg. 10). Narrow goals decrease satisfaction, even with high-quality outcomes, which have negative effects on future behavior. They can also inhibit learning and experimentation with alternative methods, undermine cooperation, and harm intrinsic motivation.

A few years ago, researchers from Harvard, Wharton, Kellogg, and the University of Arizona argued that goal setting was “overprescribed” and featured “powerful and predictable side effects” (pg. 6). While acknowledging past research demonstrates that “specific goals provide clear, unambiguous, and objective means for evaluating…performance” and thus “motivate performance far better than “do your best” exhortations” (pg. 7), the researchers found that this intensity of focus on goals can lead to tunnel vision and poor, often unethical decisions. Examples include Sears in the early 1990s, whose sales goals for its auto repair staff led to overcharging and unnecessary repairs. Revenue-based rather than profit-based goals at Enron helped lead to the company’s destruction. A challenging goal (a car “under 2,000 pounds and under $2,000”) coupled with a tight deadline at Ford in the late 1960s brought about the easily-combustible Pinto, many deaths and injuries, and expensive lawsuits. These narrow goals crowded out not only ethical behavior, but the broader purpose of the goals themselves. Quality, in essence, is often sacrificed for the quantifiable. Short-term gains are pursued rather than long-term health and growth. Furthermore, such narrow goals create “a focus on ends rather than means…[The researchers] postulate that aggressive goal setting within an organization increases the likelihood of creating an organizational climate ripe for unethical behavior“ (pg. 10). Narrow goals decrease satisfaction, even with high-quality outcomes, which have negative effects on future behavior. They can also inhibit learning and experimentation with alternative methods, undermine cooperation, and harm intrinsic motivation.Because managers and workers apply different skills, the best workers may not be the best candidates for managers. When this is the case, do firms promote someone who excels in her current position, or someone who is likely to excel as a manager? If firms promote based on current performance, then firms may end up with worse managers. Yet if firms promote based on traits that predict managerial potential, then firms may pass over higher performing workers, weakening the power of promotions to encourage workers to perform well in their current roles. Such promotion policies could also lead to perceptions of favoritism, unfairness, or that succeeding in one’s job goes unrewarded.

/board_meeting-147205270-58aa53925f9b58a3c9baec5d.jpg)